The UK’s PBSA sector is facing a structural tension that will define its next decade. For assets providing all-inclusive rents, every pound of unnecessary energy expenditure either compresses margin or feeds directly into the next pricing decision.

On one side sits the economic reality of development and operations: viable new schemes require average weekly rents of approximately £265, energy costs represent around 23% of operational expenditure, and build cost inflation shows little sign of relenting. On the other, students, particularly UK-born undergraduates, are making increasingly rational, budget-constrained choices about where they live. The least occupied en-suite rooms already cost 110% of a student’s maximum maintenance loan.

But affordability is not the only pressure building. A separate, structurally significant shift is reshaping how assets are valued and traded. With new development viability constrained and supply of new stock limited, transaction activity is increasingly focused on existing assets. The quality of an asset’s operational data, energy management, and ESG documentation is becoming central to exit readiness, not a secondary consideration. Investors and acquirers are asking harder questions. Asset owners who can answer them, with evidence, are better placed.

Supply Constraints Changing the Stakes

CBRE estimates a shortfall of approximately 620,000 PBSA beds in the UK by 2029. New development has not kept pace with demand, and build cost inflation, planning constraints, and rising financing costs mean that pipeline supply is unlikely to close that gap in the near term. The consequence is a transaction environment where existing assets trade with greater frequency, and where the performance credentials of those assets are scrutinised more than ever.

So, what does that mean? Assets that can demonstrate operational discipline, rental resilience, and evidenced performance carry a material advantage in both leasing and capital markets. Aspiration-led pricing without the operational data to back it up is a risk that sophisticated buyers and lenders are no longer willing to price generously.

The Hidden Costs That PBSA can Control

The all-inclusive model is PBSA’s defining value proposition, the simplicity of one weekly or monthly payment covering rent, utilities, and connectivity. It is also the source of one of the sector’s most material and underappreciated operational risks. According to CBRE analysis, energy accounts for approximately 23% of PBSA operational costs, excluding management fees. In electrically heated assets, common in legacy PBSA stock built between the 1960s and 1990s, that figure is frequently higher. Unlike a conventional residential landlord who passes utility costs to residents, PBSA carries that exposure entirely. Every unit of heat delivered to an unoccupied room, every thermostat running at full temperature while a student is in lectures, every building managed on seasonal scheduling rather than real occupancy: direct deductions from NOI.

What has changed is the precision with which this can now be addressed. Room-level IoT monitoring, capturing occupancy, temperature, humidity, and air quality continuously, provides a granular picture of where energy is being wasted. Smart heating controls triggered by real-time occupancy data eliminate the waste without degrading the resident experience. The technology retrofits to existing stock, and the payback periods are measured in heating seasons, not decades. Where Utopi works alongside Owners and Operators, that data flows continuously into The Utopi Platform, alerting site teams in real time when a room is running at 28°C suggesting a fault, or a cluster of unoccupied rooms is drawing energy at peak rates. The intervention is faster. Critically, the record of that intervention persists.

What are Buyers Looking For?

Exit readiness comes down to the quality of evidence an asset owner can prove in the due diligence process. Granular data that doesn’t just focus on good performance, it can prove it with real-time, historic insights. Assets that perform well under scrutiny and those that do not is increasingly determined by what has been recorded over the life of the asset, rather than what can be assembled in the weeks before a transaction.

On the technical due diligence side, institutional buyers expect more than a point-in-time survey. They want to see how the building has actually performed: how heating infrastructure has responded across a full occupancy cycle, whether faults have been identified and resolved within a reasonable window, what consumption looks like relative to comparable assets. An asset with a continuous, multi-year record of room-level energy performance and maintenance interventions can be underwritten with greater confidence and carries less execution risk than one without.

The legal and financial dimensions of that assessment draw on the same underlying data. Compliance documentation for SECR, CSRD, and sustainability-linked loan covenants depends on the monitoring infrastructure in place. Energy budgets grounded in actual consumption data are more credible than estimates. Forward NOI projections anchored in a demonstrable reduction trajectory are easier to defend at heads of terms. The Utopi Logbook consolidates that operational record into a structured asset history; timestamped, room-level, and continuous; that travels through due diligence as a coherent body of evidence rather than a collection of site records assembled under pressure.

Sustainability as an Operational Position

There is a live debate in the sector about whether ESG has become theatre – sustainability reports produced for investor relations purposes, with limited operational change underneath. The question of whether ESG is a genuine value driver or compliance wallpaper was among the most actively contested topics at industry forums entering 2026.

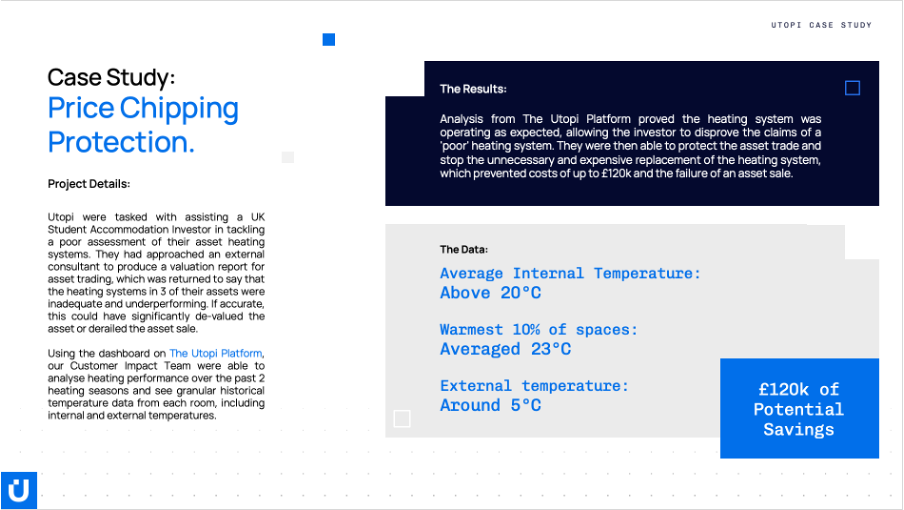

What the data – from working alongside clients across 78,000 beds in 13 countries – consistently shows is that Asset Owners treating ESG as a genuine operational discipline are the same Asset Owners who are seeing the value at exit. An Asset Manager or Operator that reduces wasted energy consumption by 15% across a portfolio of 2,000 beds reduces the utility cost base, reduces carbon intensity that investors and lenders price into financing terms, and generates the continuous data that institutional acquirers expect to find when they conduct due diligence. Utopi have experience of this already, helping one of our clients protect against price chipping at time of asset sale:

Preparing the Asset for Exit

The affordability equation will not be resolved by any single Investor decision or policy intervention. The structural undersupply crisis will persist as long as development viability remains challenged. International student policy uncertainty adds demand-side risk that is genuinely difficult to model. The tension between viable returns and affordable pricing is unlikely to disappear.

What operators can act on is the costs they control, and the operational record they are building today. Energy is the most significant controllable cost in an all-inclusive PBSA model. It is the cost most directly linked to the sustainability agenda that investors, lenders, and universities increasingly demand evidence of. And managing it well, with room-level data and smart controls responding to actual occupancy, produces the documented performance record that serves an Asset Owner at budget, at GRESB reporting, at refinancing, and at exit.

Energy efficiency investment is simultaneously an affordability strategy, a NOI protection strategy, an ESG compliance strategy, and an asset value strategy. The operational data it generates is the same dataset that underpins each of them. For assets still without the infrastructure to manage energy proactively, the cost of this is now measurable on the P&L, the rent sheet, and, at exit, the bid sheet.

For more information on how Utopi can support your ESG strategy and exit readiness, get in touch: www.utopi.co.uk/contact/.